If you’re watching a parent struggle with daily tasks and wondering how to pay for help at home, you’re not alone. Millions of families face this exact situation every year. The good news? Does long-term care insurance cover in-home care is a question with a mostly positive answer. Yes, most LTC policies do cover in-home care. But the details matter more than the headline.

This guide breaks down exactly what’s covered, what’s not, how to file a claim, and what to do when things go wrong. Think of it as the plain-English version of your loved one’s policy.

How Long-Term Care Insurance Covers In-Home Care

Most long-term care (LTC) insurance policies are built to cover more than just nursing home stays. In-home care is typically included, but coverage depends heavily on the specific policy terms.

There are two main ways a policy pays out. A reimbursement policy pays you back after you’ve already paid for care. A cash benefit policy sends you a set amount regardless of what you spend. Reimbursement policies are more common, so having a few months of savings on hand while claims are processed is a smart move.

Every policy also has a daily, weekly, or monthly benefit limit. For example, a policy might cover $180 per day. If your home aide costs $220 per day, you cover the $40 difference out of pocket.

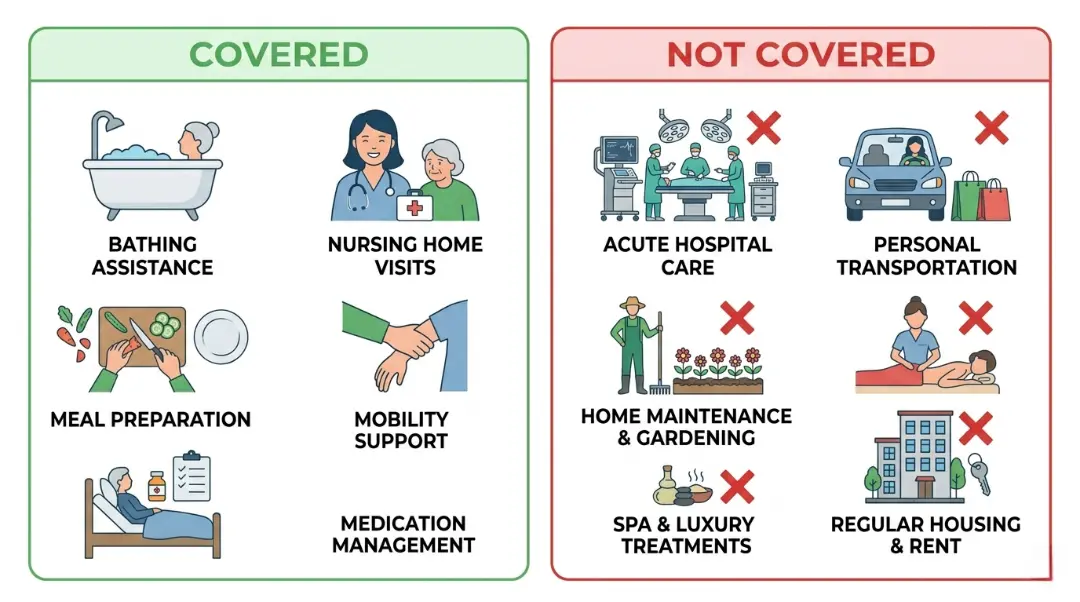

What Types of In-Home Care Services Are Typically Covered?

Most LTC policies cover both medical and non-medical in-home care services, provided eligibility requirements are met. This includes help with bathing, dressing, eating, mobility, and skilled nursing visits ordered by a physician.

Here’s a clearer breakdown:

Medical (Skilled) Care:

- Registered nurse visits

- Physical, occupational, or speech therapy

- Wound care or medication management

Non-Medical (Custodial) Care:

- Bathing, dressing, toileting

- Meal preparation and feeding assistance

- Mobility support and fall prevention

What most policies do NOT cover:

- General housekeeping not tied to a care plan

- Grocery shopping or errand running (unless part of supplemental coverage)

- Caregiver transportation costs (though some policies include mileage)

Always read the “schedule of benefits” section of the policy. That’s where the real details live.

What Are the Eligibility Triggers for LTC Benefits?

To qualify for LTC benefits, most policies require that a person needs help with at least two Activities of Daily Living (ADLs), or that a licensed professional has confirmed severe cognitive impairment such as Alzheimer’s or dementia.

The six standard ADLs are:

- Bathing

- Dressing

- Eating

- Toileting

- Transferring (moving from bed to chair)

- Continence

One thing families often miss: ADLs are more specific than they sound. Needing help getting in and out of a car doesn’t qualify as “transferring.” Needing someone to prepare meals doesn’t qualify as an “eating” impairment. The insurance company will send a registered nurse to do a home assessment. That visit determines eligibility.

If cognitive impairment is the qualifying condition, the insurer typically requires clinical evidence, such as brain imaging or a standardized test like the Mini-Mental State Examination (MMSE). Physician notes alone often aren’t enough.

[Data suggestion: Mention that roughly 70% of Americans over 65 will need some form of long-term care, per U.S. Department of Health and Human Services data. This adds urgency and relevance.

Understanding the Elimination Period (The Waiting Period Nobody Talks About)

Before benefits kick in, most LTC policies have an elimination period, which is essentially a deductible measured in time rather than money. It typically runs 30 to 100 days, with 90 days being the most common.

During this period, your family pays out of pocket for care. After the elimination period ends, the insurance company starts paying. In many cases, benefits are applied retroactively to when care began.

Here’s what to do during the waiting period:

- Use Medicare’s limited skilled care coverage if applicable

- Look into Medicaid waiver programs if income qualifies

- Pull from savings or a health savings account (HSA)

Once the benefit period begins, most policyholders no longer pay premiums. That monthly premium cost frees up cash for other needs.

Can You Use Long-Term Care Insurance to Pay for a Home Health Aide?

Yes, LTC insurance can pay for a licensed home health aide as long as they work for a licensed home care service and the policy covers custodial care. Some policies have features of cash benefits that allow policyholders to recruit on their own without agency limitations.

If your insurance requires an agency, contact the insurer first and check that the agency you choose is an approved provider. Home care organizations that accept LTC insurance will usually do most of the claims paperwork for you, which relieves a lot of load off the family.

Can a Family Member Be Paid as a Caregiver Under LTC Insurance?

This is one of the most common questions, and the answer isn’t simple. Cash benefit policies generally allow it because the policyholder receives money directly and can use it as they choose. Reimbursement policies typically don’t, since they require invoices from licensed providers.

There’s another catch: using a family caregiver during the elimination period may affect how those days are counted toward your waiting period. Check this detail with the insurer before making any arrangements.

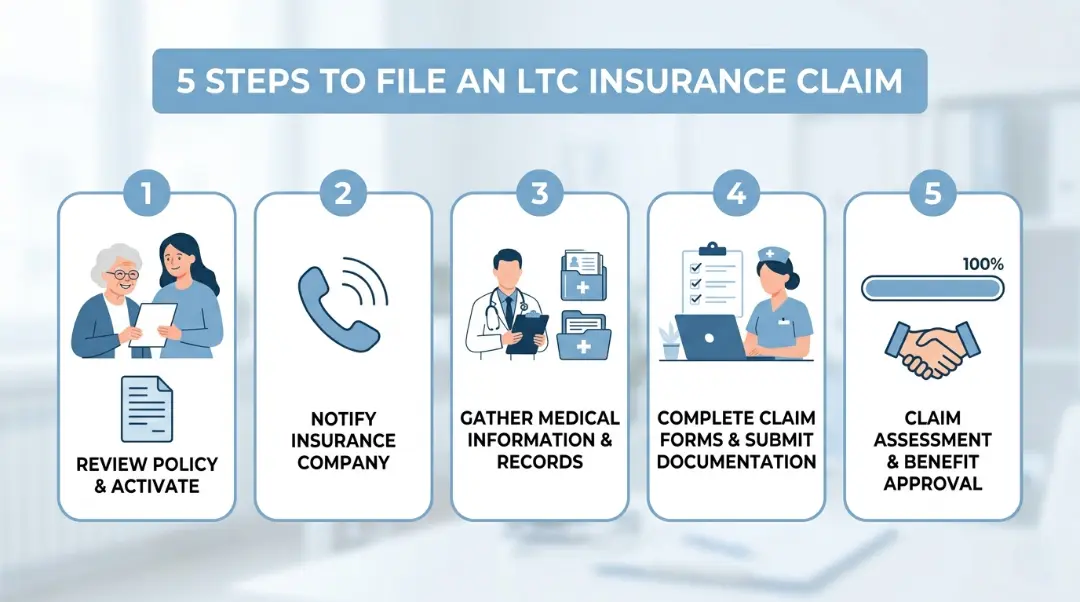

Step-by-Step: How to File a Claim for In-Home Care

Filing an LTC claim isn’t complicated, but small mistakes lead to denials. Follow these steps carefully.

Step 1 Review the policy.

Understand the benefit amount, elimination period, and whether the policy reimburses or pays cash.

Step 2 Get a physician’s assessmen

The doctor needs to document that care is medically necessary and identify which ADLs the person cannot perform.

Step 3 Choose a licensed home care agency.

Confirm with the insurer that the agency is approved. Agencies that accept LTC insurance often have dedicated staff to help with claims.

Step 4 Submit the claim form.

Include the completed claim form, medical records, and the home care agency’s invoices. Missing information is the most common reason for denial.

Step 5 Monitor and follow up.

Keep a log of all submitted claims, payments received, and any correspondence with the insurer.

Common Myths About Long-Term Care Insurance

Myth 1: Medicare covers in-home personal care. Medicare covers skilled home health services, like nursing visits and therapy, but it does not cover custodial care (bathing, dressing, eating). The hours are also limited, and you can’t choose your agency.

Myth 2: LTC insurance covers everything. It covers what the policy says it covers, up to the benefit limit. Supplemental benefits like home modifications or durable medical equipment may be included, but they come with their own rules.

Myth 3: Premiums are your only cost. The elimination period means you’ll pay out-of-pocket before benefits begin. Factor this into your planning.

What to Do If Your Claim Is Denied

Denials happen, often for small reasons. A care plan might list assistance with two ADLs, but if the caregiver’s invoice only documents one, that day’s claim gets rejected.

Here’s how to respond:

- Request a written explanation from the insurer. They’re legally required to provide one.

- Gather complete documentation from the home care provider, including detailed service logs.

- File a formal appeal within the deadline stated in the denial letter.

- Contact your state’s Department of Insurance if the denial seems unfair or is taking too long.

- Consult an elder law attorney for complex denials, especially those involving cognitive impairment.

Alternatives When LTC Insurance Doesn’t Cover Everything

- Medicaid waiver programs can cover custodial in-home care for qualifying low-income individuals

- VA benefits for veterans can supplement or replace LTC insurance entirely

- LTC insurance tax deductions premiums are often partially deductible; consult a tax advisor

- Inflation protection riders on newer policies help benefit amounts keep up with rising care costs

Finding Trusted Home Care Near You

If you’re looking for home care services in Denver or the surrounding area, Castle Pines Home Care offers licensed, compassionate in-home care that works directly with LTC insurance policies. Our team handles the paperwork, coordinates with insurers, and makes sure your loved one gets the care they’ve earned.

Contact us today to learn how we can help your family navigate LTC insurance and get care started quickly.

Frequently Asked Questions

Does long-term care insurance cover in-home care for dementia patients?

Yes. Severe cognitive impairment, including Alzheimer’s and dementia, is a standard eligibility trigger in most LTC policies. Clinical documentation and a home nurse assessment are typically required.

What is the elimination period in LTC insurance?

It’s a waiting period, usually 30–90 days, during which you pay out of pocket before benefits begin. Most policies backdate payments to the start of care.

Can LTC insurance pay a family member caregiver?

Cash benefit policies typically allow this. Reimbursement policies usually require invoices from a licensed agency.

Does private insurance cover home health care?

Some private health insurance plans cover skilled home health care after a hospitalization, but they rarely cover long-term custodial care. LTC insurance is specifically designed for that purpose.

What home care benefits does Medicare typically not cover?

Medicare does not cover ongoing personal care, such as bathing, dressing, or companion care. It only covers short-term skilled care tied to a medical condition.