Home health care bills add up fast. If you or a loved one is receiving care at home, you’re probably wondering whether any of those costs can come off your taxes. The short answer is: yes, some of it can, but not all of it. Whether home health care is tax deductible depends on the type of care provided, who’s paying for it, and how your income looks on paper.

This guide breaks it all down in plain language. We’ll cover exactly which services qualify, who can claim the deduction, how to calculate it, and what most people miss when filing. By the end, you’ll know where you stand and what steps to take next.

When Is In-Home Care Tax Deductible?

In-home care is tax deductible when the services are medically necessary, prescribed by a doctor as part of a formal care plan, and the total unreimbursed medical expenses exceed 7.5% of your adjusted gross income (AGI). The care also can’t be reimbursed by Medicare, Medicaid, or private insurance.

The IRS lays out these rules clearly in Publication 502. Three conditions must all be true at the same time:

- The care is part of a physician’s documented care plan

- Your total qualifying medical expenses go above 7.5% of your AGI

- None of those expenses were paid back by insurance or government programs

If all three boxes are checked, you have a real deduction on the table.

There’s also an important exception for people with chronic illness. If a licensed health care practitioner certifies that someone has severe cognitive impairment or has lost the ability to perform at least two activities of daily living (ADLs) for 90 days or more, then even personal and household care becomes tax deductible. This is a key rule that many families miss entirely.

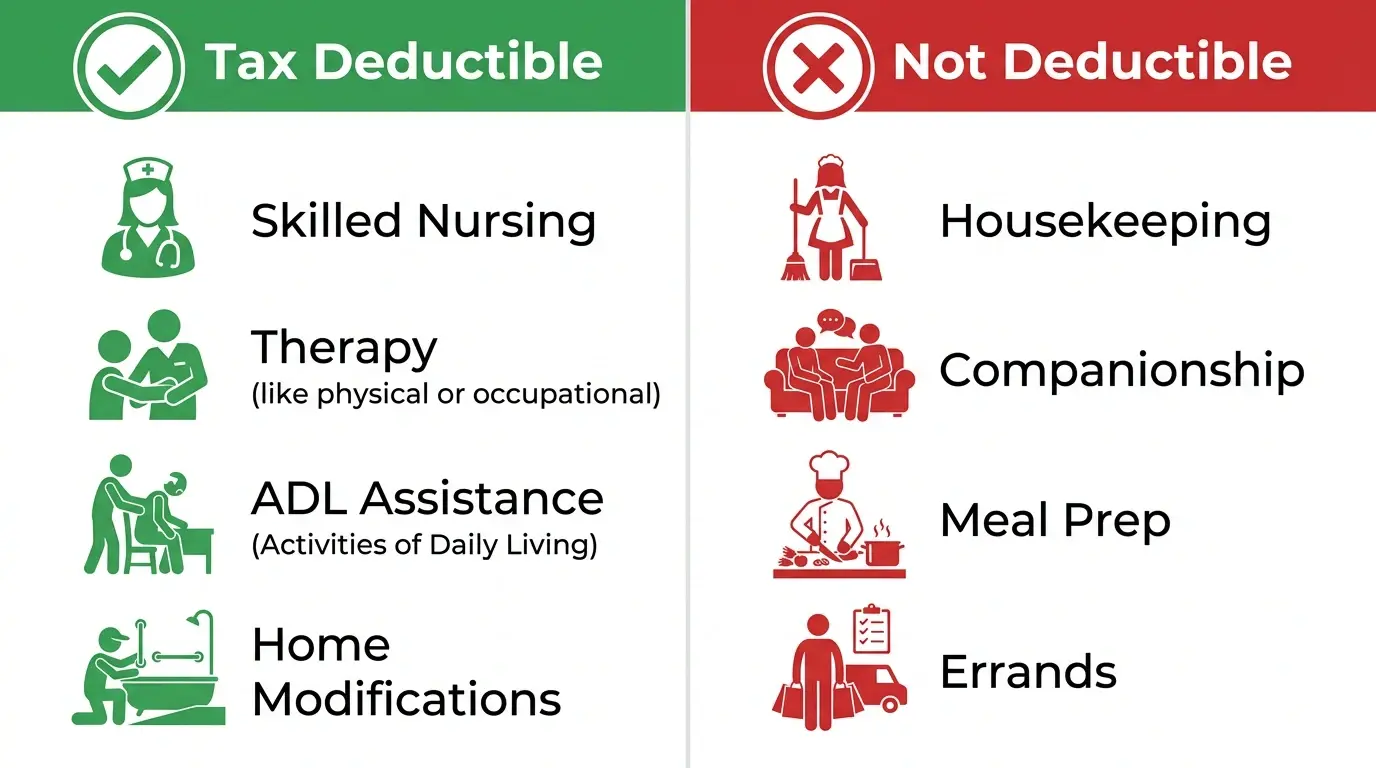

Home Care and Home Health Care Expenses That Are Tax Deductible

Medically necessary home health care services are generally tax deductible. This includes skilled nursing care, physical therapy, occupational therapy, speech therapy, and doctor-prescribed help with activities of daily living like bathing, dressing, and mobility assistance.

Here’s a practical breakdown:

| Service | Tax Deductible? |

| Skilled nursing care | Yes |

| Physical, occupational, speech therapy | Yes |

| Help with ADLs (if prescribed) | Yes |

| Medical equipment used at home | Yes |

| Home modifications (ramps, grab bars) | Yes |

| Housekeeping and cleaning | No |

| Companionship visits | No |

| Meal preparation | No |

| Running errands | No |

The IRS draws a clear line between medical care and personal comfort. If the service doesn’t connect directly to a diagnosed condition or a doctor’s care plan, it doesn’t qualify.

Also worth knowing: certain home modifications can be deducted as medical expenses. Building entrance ramps, widening doorways, adding bathroom grab bars, and lowering countertops all qualify, as long as they’re for medical reasons and not meant to increase your property’s value.

Home Care Services That Aren’t Tax Deductible

Home care services that are not tax deductible include general housekeeping, laundry, grocery shopping, meal preparation, companionship, and non-medical transportation. The IRS views these activities as standard personal, living, or family expenses rather than direct treatments for a medical condition.

The federal government explicitly blocks deductions for the following tasks:

- Companionship Visits: Paying someone to sit with a senior, talk, watch television, or provide social interaction.

- Housecleaning and Maintenance: Standard maid services, vacuuming, dusting, doing laundry, or mowing the lawn.

- General Meal Preparation: Cooking regular family meals, even if the caregiver prepares them specifically for the patient.

- Chauffeur Services: Driving a senior to social events, family visits, or grocery stores.

| Care Service Type | Tax Deductible? | IRS Code Source |

| Skilled Nursing (Wound Care, Vitals) | Yes | IRS Publication 502 |

| Physical or Speech Therapy | Yes | IRS Publication 502 |

| Help with Bathing and Eating (Prescribed) | Yes | IRS Publication 502 |

| Housekeeping and Laundry | No | IRS Publication 502 |

| General Companionship | No | IRS Publication 502 |

Who Can Deduct Home Care Expenses on Their Taxes?

The person receiving care can deduct qualifying expenses on their own return. A family member, such as an adult child, can also deduct those expenses if they paid for more than half of the care recipient’s annual support and the person receiving care qualifies as their dependent.

The IRS spells out the relationship rules in Publication 502. Qualifying relatives include adult children, siblings, stepparents, grandparents, aunts, uncles, and in-laws. You don’t have to live with the person to claim them as a dependent.

To claim a parent as a dependent, three things need to be true:

- You cover more than 50% of their total annual support

- Their gross income falls below the IRS threshold (for 2025, that’s $5,050)

- They’re a U.S. citizen, resident, or qualifying nonresident

If you meet these requirements, claiming a parent as a dependent can also open doors to other tax benefits, including the Credit for Other Dependents and potentially the Child and Dependent Care Credit.

One important note on family caregivers: if you pay a family member to provide care, that’s only deductible if the family member is not your spouse or your own dependent. Those payments are also subject to payroll tax rules and must be reported as income by the caregiver.

Understanding Home Care Tax Deductions

Home care tax deductions fall under the medical expense deduction on Schedule A of your federal tax return. You must itemize your deductions to claim them, which means the standard deduction won’t apply. For 2025, the standard deduction is $15,000 for single filers and $30,000 for married couples filing jointly.

This matters more than people realize. If your total itemized deductions, including medical expenses, mortgage interest, and state taxes, don’t exceed the standard deduction, itemizing won’t benefit you. A tax professional can run the numbers both ways to see which path puts more money back in your pocket.

Also note: are health care premiums tax deductible? In some cases, yes. If you pay out-of-pocket health insurance premiums that aren’t covered by an employer or government program, those can be added to your total medical expense deduction, which may push you past the 7.5% AGI threshold.

FSA and HSA A Often-Overlooked Option

This is a gap that most articles on this topic skip right past. If you have a Flexible Spending Account (FSA) or Health Savings Account (HSA), you may be able to pay for qualifying home health care expenses with pre-tax dollars. That means you’re reducing your taxable income before you even file. FSA and HSA funds can typically cover:

- Skilled nursing care

- Prescribed therapy services

- Medical equipment used at home

Using an FSA or HSA for home care costs is one of the most straightforward ways to get a tax break, even if you don’t itemize.

How to Claim Home Care Deductions

To claim home care deductions, you must file Schedule A with your federal tax return and list your qualifying medical expenses under the Medical and Dental Expenses section. You cannot claim this deduction if you take the standard deduction.

Here’s what you need to have on hand when filing:

- Invoices and receipts for all care services

- A written care plan from a licensed physician or health care practitioner

- A chronic illness certification (if applicable)

- Daily activity logs from caregivers showing time spent on medical vs. non-medical tasks

- Records of any reimbursements from Medicare, Medicaid, or insurance

If you hired an in-home caregiver directly as a household employee, IRS Publication 926 may allow you to deduct certain employer taxes you paid on their behalf, such as Social Security tax and state employment taxes. This doesn’t apply if you hired through an agency since the caregiver is legally the agency’s employee in that case.

What If You Don’t Itemize?

If the standard deduction makes more financial sense for you, you still have options. Beyond the FSA/HSA route mentioned above, check whether your state offers its own medical deduction. Several states have lower AGI thresholds or separate rules that can work in your favor even when the federal itemized deduction doesn’t.

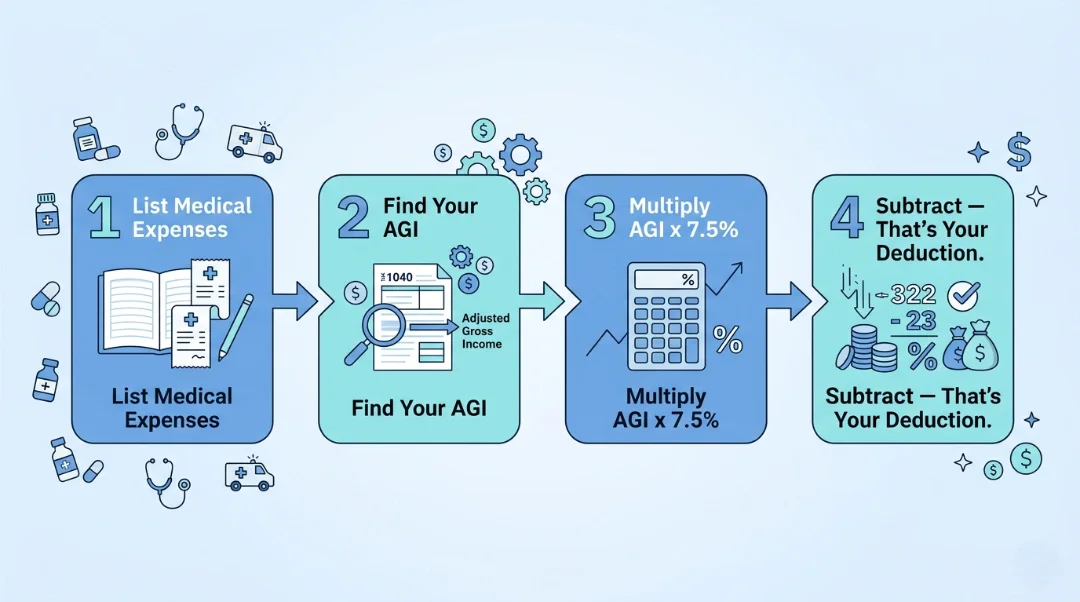

How to Calculate Your Home Health Care Tax Deduction

To calculate your home health care tax deduction, add your qualified care costs, determine your adjusted gross income, find 7.5% of that income, and subtract it from the costs. Only the dollar amount that sits above that 7.5% baseline can be deducted from your federal taxable income.

Let’s walk through the math step by step:

Step 1: Total Your Qualified Medical Expenses

Gather your receipts for nursing care, certified aides, modifications, and prescriptions. For this example, let’s say your total qualified care cost equals $20,000 for the year.

Step 2: Find Your Adjusted Gross Income (AGI)

Look at your federal tax return to find your AGI. This is your total gross income minus specific adjustments like retirement contributions. Let’s assume your AGI is $80,000.

Step 3: Calculate the 7.5% IRS Threshold

Multiply your AGI by 7.5% to find the baseline hurdle. $$$80,000 \times 0.075 = $6,000$$ The first $6,000 of your medical costs cannot be deducted.

Step 4: Subtract the Threshold from Your Total Costs

Subtract your baseline hurdle from your total qualified expenses to get the final deduction amount. $$$20,000 – $6,000 = $14,000$$ You can write off $14,000 on your Schedule A form.

Tax Deduction vs. Tax Credit: What’s the Difference?

A tax deduction reduces your taxable income, which indirectly lowers the taxes you owe. A tax credit directly reduces the amount of tax you owe, dollar for dollar. Credits are generally more valuable than deductions.

Think of it this way. A $1,000 deduction saves you money based on your tax bracket. If you’re in the 22% bracket, that deduction saves you $220. A $1,000 credit saves you a flat $1,000, regardless of your bracket.

For home care, most of what we’ve discussed falls under deductions. But if you’re paying for care to allow yourself (or a spouse) to work or look for work, you may also qualify for the Child and Dependent Care Credit. This credit applies when a qualifying person, which includes a dependent who is physically or mentally unable to care for themselves, requires care so you can be employed.

It’s worth checking both angles with a tax professional. The health care premium deduction, for example, may work differently if you’re self-employed versus a traditional employee. Self-employed individuals can often deduct 100% of their health insurance premiums as an above-the-line deduction, which doesn’t require itemizing at all.

Final Thoughts

Figuring out is home health care tax deductible isn’t always a simple yes or no. It depends on what type of care is being provided, who’s paying for it, and how the numbers stack up against your income. The good news is that between the medical expense deduction, FSA/HSA options, and potential state-level rules, there are real opportunities to reduce what you owe.

If your loved one is dealing with dementia-related behavioral changes alongside their care needs, our article on What Stage of Dementia Is Anger? may also be a helpful read as you plan their care.

At Castle Pines Home Care, we work with families every day who are navigating both the emotional and financial sides of in-home care. If you’re looking for home care services in Denver and want to understand your options, we’re here to help. Contact us today to talk through what care might look like for your family.

Frequently Asked Questions

Is paying a family member for home care tax deductible?

Yes, in some cases. You can deduct payments made to a family member caregiver as long as they are not your spouse or your own dependent. Those payments must follow payroll tax rules and be reported as income by the caregiver.

Can I deduct home care for a parent who doesn’t live with me?

Yes. You can claim a parent as a dependent even if they live elsewhere, as long as you provide more than half of their annual support and they meet the IRS income and citizenship requirements.

Is home health care the same as long-term care for tax purposes?

Not exactly. Home health care refers to medically necessary services provided at home. Long-term care is a broader category that can include custodial care for chronically ill individuals. Both can be deductible under certain conditions, but the qualifying criteria differ slightly.

Does Medicare or Medicaid affect my deduction?

Yes. Any expenses reimbursed by Medicare, Medicaid, or private insurance cannot be deducted. Only unreimbursed out-of-pocket costs count toward your medical expense deduction.

Can I use an FSA or HSA for home health care costs?

Yes. Qualifying medically necessary home health care expenses, including skilled nursing, prescribed therapy, and medical equipment, can typically be paid with FSA or HSA funds, giving you a tax advantage without needing to itemize.

Are health care premiums tax deductible?

In many cases, yes. If you pay out-of-pocket health insurance premiums that aren’t subsidized by an employer or government program, they can be included in your total medical expense deduction on Schedule A. Self-employed individuals may deduct 100% of premiums without itemizing.