Nursing home care is costly and when a family member needs it the financial pressure hits hard. You’re not alone if you’re trying to figure out how to pay for nursing home care with social security. This is precisely the dilemma that millions of families face every year, not knowing if Social Security benefits would be sufficient, or what other programs can step in to cover the gap.

The short answer is: Nursing home fees can be paid for with Social Security retirement, SSDI and SSI benefits. But in most circumstances they will not be paying the entire price alone. The good news is that most seniors can get the care they need without paying fully out of pocket when Social Security is combined with Medicaid, Veterans benefits, or other programs.

How to Use Social Security to Pay for a Nursing Home Stay

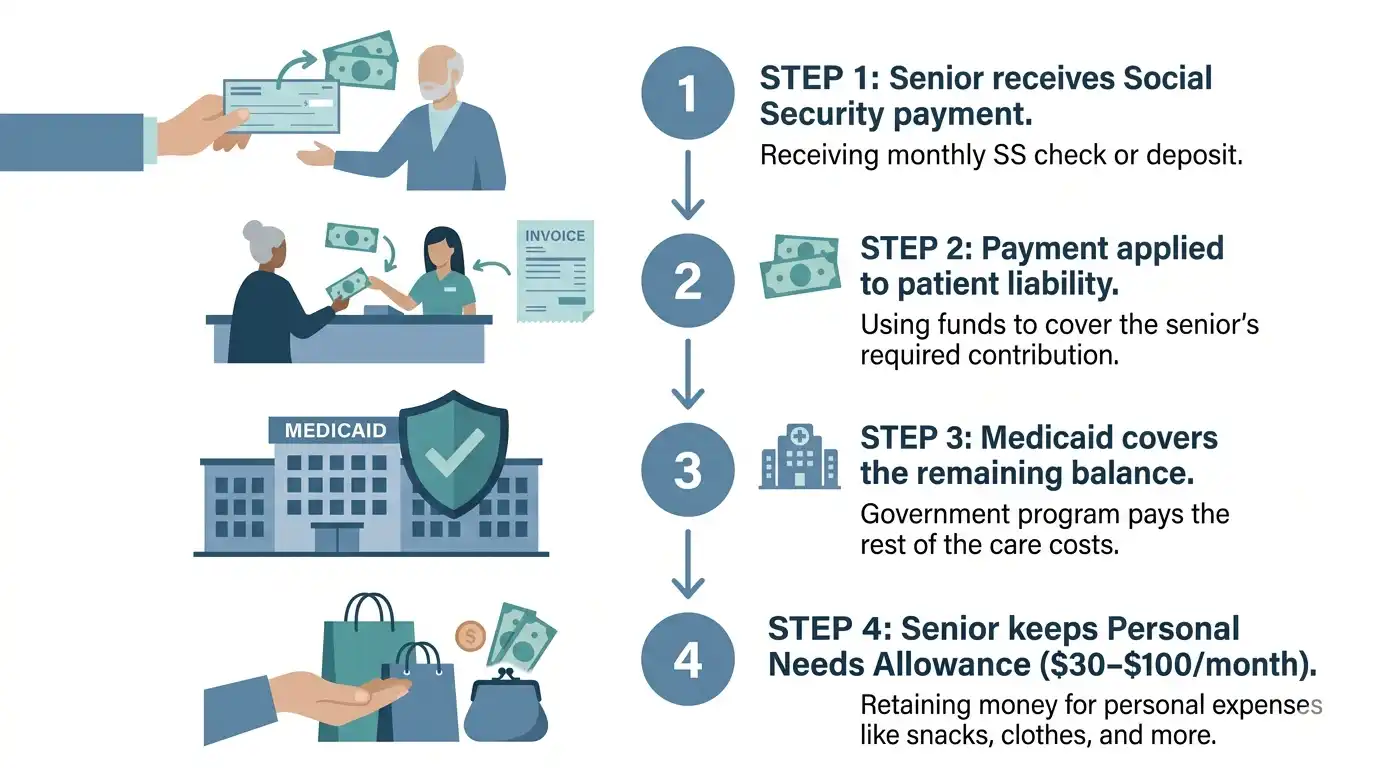

Social Security doesn’t write a check directly to a nursing home. Instead, benefits are paid to the recipient, who then uses those funds toward their care costs. There are four types of Social Security benefits that apply here:

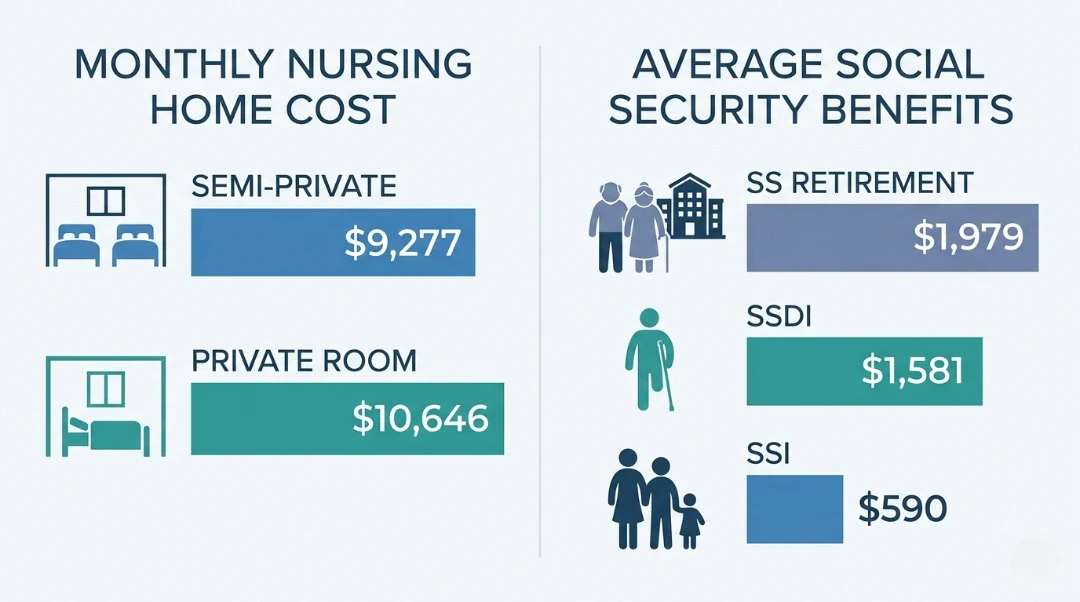

- Social Security Retirement For workers aged 62 and older who paid into the system. The average monthly payment in 2025 is $1,979.

- Social Security Disability Insurance (SSDI) For people who can no longer work due to a disability. Average monthly benefit in 2025: $1,581.

- Supplemental Security Income (SSI) For low-income seniors aged 65+ and disabled individuals. Average monthly payment: $590.

- Optional State Supplements (OSS) Some states add extra payments on top of SSI. These vary widely by state and may be paid directly to the nursing facility.

A person can receive more than one type of benefit. For example, if your loved one’s total monthly income including Social Security retirement is below $987 in 2025, they may qualify for SSI on top of their retirement benefit.

How Much Does Nursing Home Care Actually Cost?

Before planning how to pay for it, you need to know what you’re up against.

According to Genworth’s 2024 Cost of Care Survey, the national median monthly cost for nursing home care is:

- $9,277/month for a semi-private room (~$111,325 per year)

- $10,646/month for a private room (~$127,750 per year)

Costs vary dramatically by state. Louisiana averages around $7,483/month for a semi-private room, while Alaska can exceed $30,371/month. States like Connecticut, Massachusetts, and Hawaii regularly surpass $14,000/month.

So how much of that does Social Security actually cover? Let’s run the numbers:

| Benefit Type | Avg. Monthly (2025) | % of Semi-Private Room Covered |

| SS Retirement | $1,979 | ~21% |

| SSDI | $1,581 | ~17% |

| SSI | $590 | ~6% |

SSI covers the least on its own but SSI recipients usually qualify for Medicaid, which pays 100% of nursing home costs once eligibility is confirmed.

Social Security vs. Supplemental Security Income: What’s the Difference?

The specific rules governing nursing homes and social security depend entirely on which program sends the monthly check.

| Benefit Type | How Nursing Homes Handle the Check | What You Keep |

| Retirement / SSDI | Stays at the full monthly amount, but the vast majority goes to the facility bill. | Nothing is legally mandated unless Medicaid steps in. |

| SSI (Without Medicaid) | Stays at the standard rate (around $994 max) to pay the private facility rate. | The individual controls the full amount until it runs out. |

| SSI (With Medicaid) | Drops to a strict token amount after a stay crosses the 90-day mark. | The senior keeps exactly $30 per month as a personal allowance. |

If your family member relies on SSI and stays in a facility paid for by Medicaid for over 90 days, the government slashes that SSI check down to just $30 a month. This small sum is the federal Personal Needs Allowance, meant for small comforts like haircuts or clothing.

However, if a doctor signs Form SSA-186 stating the stay is temporary (90 days or less) and the senior will return home, the government will maintain the full monthly payment.

Will Social Security Be Reduced While in a Nursing Home?

Yes, but only if Medicaid pays for the stay and the person is on SSI. If so, SSI will be cut back to $30 a month. This is sometimes called the “SSI nursing home rule.” It starts after 90 days of Medicaid-paid care. Social Security retirement benefits and SSDI benefits are not cut.

If your loved one stays 90 days or less or if Medicaid isn’t covering the expense, SSI isn’t immediately cut. For shorter stays, your loved one and his doctor can fill out form SSA-186 for continued full SSI benefits.

If you are on SSDI or ordinary Social Security retirement, your payments will not stop because of how long you stay in the nursing facility.

Can a Nursing Home Take Your Social Security Check?

No. A nursing home cannot legally seize a patient’s Social Security benefits, pension, or other income. Federal law protects these payments. The only exception is if the account is in default and a collection agency has been involved in that case, funds may be used to satisfy outstanding bills.

That said, when Medicaid covers the care, most of a resident’s monthly income including Social Security is applied toward the nursing home bill. Medicaid allows residents to keep a small Personal Needs Allowance (PNA), typically between $30 and $100/month depending on the state. This pocket money is for personal expenses like toiletries, a haircut, or a magazine.

If a community spouse (a husband or wife still living at home) is involved, additional protections apply. A portion of income may be set aside for the spouse under what’s called the Minimum Monthly Maintenance Needs Allowance (MMMNA), which helps prevent financial hardship for the non-institutionalized partner.

How Social Security Works When Medicaid Takes Over

Medicaid funds roughly two-thirds of all institutional care across the country. When an aging adult runs out of private funds and applies for this state aid, the rules surrounding their monthly income change completely.

Understanding Patient Liability and Income Caps

Medicaid requires residents to contribute almost all their monthly income toward their own care costs. This calculated share is called patient liability. If your parent receives $2,000 from retirement, they cannot keep that cash. Medicaid will pay the facility its standard daily rate, but it orders the senior to hand over their check to help offset that cost.

Furthermore, many states enforce a strict gross income limit of $2,982 per month for long-term care applicants. If a senior’s monthly checks total $3,100, they are technically over-income and face immediate denial.

The Miller Trust Solution

To bypass this income barrier, families must work with an elder law expert to establish a specialized legal account.

This structural framework is a Miller Trust, also known as a Qualified Income Trust (QIT). By routing the excess income through this specific legal vehicle, the state discounts the overage, allowing the senior to qualify for care.

Protecting the Healthy Spouse at Home

The law includes protections so the healthy spouse living at home does not end up broke. Under the Minimum Monthly Maintenance Needs Allowance (MMMNA) guidelines, the state allows the healthy spouse to keep a portion of the applicant’s income.

If the at-home spouse earns very little, a calculated slice of the senior’s monthly check is legally transferred to them instead of going to the care facility. The state also sets a Community Spouse Resource Allowance (CSRA), which lets the independent spouse protect a maximum of $162,660 in joint savings.

Is a Nursing Home the Right Option if Funds Are Limited?

Not always. For seniors without substantial savings, there are alternatives worth considering before committing to a nursing home.

- Assisted living Less intensive care, typically lower cost. Average monthly cost: ~$5,350 (Genworth 2024).

- In-home care For seniors who can live safely at home with some help. This can be covered by Medicaid waiver programs in many states.

- Memory care Specifically for Alzheimer’s and dementia patients. Usually priced similarly to nursing homes.

- Adult day programs A lower-cost daytime care option that allows seniors to stay home at night.

Social Security benefits can be applied toward any of these options, not just nursing homes. Medicaid home and community-based services (HCBS) waivers in many states also cover in-home care, which lets seniors avoid facility placement entirely.

Other Ways to Pay for Nursing Home Care

Because regular retirement checks rarely cover modern facility rates, families must explore alternative funding avenues to bridge the massive gap.

- Medicare Skilled Nursing Coverage: This federal program pays 100% of the costs for the first 20 days after a three-day hospital stay. Days 21 through 100 require a daily co-pay of $217, and all coverage stops completely after day 100.

- Veterans Aid and Attendance: This special pension program provides additional tax-free monthly income to wartime veterans or surviving spouses who need help with daily living activities.

- Long-Term Care Insurance: Private policies help fund care if purchased decades before health issues arise, though premium hikes can strain fixed budgets.

- Home Equity Options: Families frequently sell the family home, lease it out for monthly income, or utilize a reverse mortgage to generate immediate care cash.

How to Legally Manage a Loved One’s Social Security Benefits

When a senior experiences cognitive decline from conditions like dementia, they lose the ability to manage their own billing accounts. Families must establish legal authority to handle the incoming money.

1.Establish Power of Attorney:Prerequisite Step.

Have the senior sign a durable financial Power of Attorney (POA) while they still possess legal capacity. This grants you the power to manage private bank accounts and pay monthly facility bills.

2.File Form SSA-11 with the Government:Required for Federal Funds.

Be aware that the federal government does not recognize a standard POA for managing monthly benefits. You must file Form SSA-11 directly with the local office to become an official Representative Payee.

3.Open a Dedicated Payee Account:Banking Setup.

Set up a specific bank account titled along the lines of “[Senior’s Name] by [Your Name], Representative Payee.” This keeps federal benefits completely separate from your personal cash.

4.Direct the Monthly Deposits:Final Activation.

Route the monthly checks into this new account. Use these funds exclusively for the senior’s care costs, keeping careful records for annual government reports.

Does Social Security Pay for Other Senior Living Options?

Yes. Social Security benefits can be used to pay for assisted living, memory care, in-home care, and adult day services not just nursing homes. There is no rule restricting Social Security payments to nursing facility use only.

Many families find that assisted living or in-home care is a better fit financially. The monthly costs are lower, and Social Security benefits go further. If your loved one qualifies for SSI, they likely also qualify for Medicaid home and community-based services, which can fund in-home personal care in most states.

For families in Colorado, our team at Castle Pines Home Care provides professional, compassionate in-home support that allows seniors to stay in their own homes longer. If you’re weighing nursing home placement against in-home care, our home care services in Denver can be a meaningful alternative often at a fraction of the nursing home cost.

Step-by-Step: What to Do When Social Security Isn’t Enough

If your family is in this situation right now, here’s a practical starting point:

- List all income sources Social Security, pensions, retirement accounts, savings.

- Contact your state Medicaid office Ask about income and asset limits. Apply early. The process takes time.

- Consult an elder law attorney Especially if assets exceed Medicaid limits. Proper planning can protect a spouse’s finances.

- Apply for Veterans benefits If your loved one served during wartime, the Aid and Attendance benefit could add hundreds per month.

- Review any existing insurance policies Long-term care, life insurance with LTC riders, or annuities.

- Tour nursing homes and request itemized price sheets Know exactly what you’re paying for before signing anything.

Starting this process six to twelve months before care is needed gives your family the most options. Last-minute Medicaid applications during a crisis are stressful and sometimes result in coverage gaps.

Final Thoughts

Figuring out how to pay for nursing home care with social security is one of the most stressful financial challenges a family can face. The costs are real, and the paperwork feels endless. But the options exist Social Security, Medicaid, Veterans benefits, Medicare, and private insurance can all play a role.

The smartest move is to start planning before a crisis hits. Talk to an elder law attorney. Apply for every benefit your loved one qualifies for. And if in-home care is a viable option, it’s often a better financial and emotional choice than a nursing home.

If you’re in the Denver area and exploring alternatives to nursing home placement, contact Castle Pines Home Care today. We help families find the right level of care at the right cost.

Frequently Asked Questions

Can Social Security be garnished for nursing home bills?

No. Social Security payments are protected from garnishment under federal law. A nursing home cannot seize or freeze a patient’s Social Security deposits unless an account is in default and the debt has gone to collections.

What is the $30 SSI rule for nursing homes?

When Medicaid pays for a nursing home stay lasting more than 90 days, the resident’s SSI benefit is reduced to $30 per month. This rule exists because Medicaid is already covering most living expenses. The resident keeps the $30 as personal spending money.

Does Medicare pay for long-term nursing home care?

No. Medicare covers short-term skilled nursing care only up to 100 days after a qualifying hospital stay. After that, families must find another payment source. Medicare was never designed to cover custodial, long-term nursing home stays.

How long will Medicaid pay for nursing home care?

Indefinitely, as long as the resident continues to meet the eligibility requirements (income, assets, and level-of-care criteria). There is no cap on duration for Medicaid nursing home coverage.

What is the Medicaid 5-year look-back period?

Medicaid reviews any asset transfers made within five years of the application date. Transfers made to reduce assets and qualify for Medicaid faster can result in a penalty period during which Medicaid won’t cover costs. An elder law attorney can help you avoid common mistakes.